ATTENTION LANDLORDS AND PROPERTY MANAGERS

If you have failed at creating financial security for yourself through any type of rental real estate in the past, it’s not your fault. There is a lot of information out there, and it can be confusing and overwhelming. Many times, it’s that information overload that keeps you from success. It’s okay, we are going to fix that today.

Also, if you have been concerned in the past that you just can’t achieve financial freedom and financial security through rental real estate, I want to put those fears to rest. You can do this. You just need the right person to explain it to you.

Your competitors want you to think that rental returns are really low, that being financially free without owning hundreds of rentals is next to impossible, that managing real estate is ridiculously intense, and you need to be on call 24/7 for your demanding tenants. I’m here to tell you they’re wrong. They have their own reason for wanting you to think that, but it’s not true.

And regardless of what the mainstream media wants you to believe, signs of economic uncertainty are everywhere. Reports show that unemployment is rising, and companies continue to lay off employees as they quietly prepare for an economic downturn.

The rapid rise of AI and automation is not helping the unemployment situation either.

Household savings are at an all-time low, and personal credit card debt is at an all-time high. According to a new report from Lending Club, as of January 2023, 60% of U.S. adults, including more than four in 10 high-income consumers, live paycheck to paycheck.

Rising unemployment means more income uncertainty for landlords who rely on that rent.

And if you haven't noticed, many local governments have quietly been passing pro-tenant laws and increasing squatter rights.

So, when your tenants decide not to pay their rent when they lose their jobs, going to court, getting them out of the property, and collecting back rent will require way more work and squeeze your cash flows and resources even further. Tenants now face almost no consequences when they don't meet their rental obligations. All the current and new changes creeping in will seriously hurt an investor's bottom line.

You want to do good. You want to help the situation and provide good quality housing to your tenants. But it becomes very difficult when the odds are against you, and you get punished instead of rewarded for your work.

I know you have a dream of becoming financially secure while having a positive impact on the world, and I want to show you how to make that happen.

So, if you are a landlord or property manager who wants predictability and income security in your rental portfolio during these uncertain times, you will learn how to do that.

Or, if you are just getting started and thinking of buying your first rental property to supplement your income from the stock or crypto market, or if you are looking to replace the income from your job completely, you will learn how to do that.

My goal here is to show you that Investing in Section 8 Rentals is the secret to financial security in these uncertain times, and I am going to show you my proprietary frameworks that will make it simple for you to achieve that result. But first, let's briefly talk about why you should listen to me.

WHY LISTEN TO ME

Hi, my name is Suhail. Just like you, I actively buy, hold, and manage income-producing real estate. The income is then used to pay for my monthly expenses. I have been involved in the industry for over two decades and operate cash-flowing rental real estate in high- and low-priced areas.

I know firsthand how stressful it is for landlords and property managers who screen and manage tenants, maintain properties, process evictions, secure vacant properties, and collect unpaid rent.

What I also know is how to eliminate most of those headaches, maximize the return on my investment, manage the property to get the highest rents, and optimize my cash flow.

Here is an example of one of my client's out-of-state investments. It is a triplex located in Cleveland, Ohio, that I helped them acquire, renovate, stabilize, and rent out to Section 8 tenants. They used my frameworks to be able to find an asset that would work for their holding timelines and the amount of work they were willing to put into it.

The property was purchased for $54,000, and another $50,000 was invested in the sustainable renovation. At acquisition, the rents were $960 per month. When we were done stabilizing the place three months later, the property generated $2,877 a month through Section 8, when the average market rents were $2,200. You can see the renovation in the photos and the government lease contracts as proof and also do the math on the return on investment if you choose.

Here is another example of one of my client's properties in Hollister, California.

This deal was purchased subject to the existing liens, and the plan was to renovate and resell it. Well, at the end of 2022, the rates spiked, and the market froze. Instead of dropping the asking price and freaking out, with my guidance, my clients could pivot quickly and get a Section 8 tenant in there for $3,124 when the average market rents were only $2,700 a month. That's $400 more in monthly cashflow.

Now, they can easily continue paying down the underlying debt and wait until they find a suitable buyer or come back to the market to sell the property when the rates come down. Actually, they may end up selling it to the Section 8 tenant. Yes, that is correct. They now have programs allowing tenants to become owners instead of renters, and my clients and I are providing that chance to tenants who would be interested in such an opportunity.

In this rapidly changing market, you must be able to pivot quickly to protect your downside. You can see the renovated property in the photos and the government lease contract as proof. The trick is to buy correctly and with proper guidance.

Here is one of the deals I recently did in Fairfield, California. I acquired the property with 100% seller financing and renovated the place for about $25,000.

The average market rent in this area is $2,575 a month. I rented this property out for $2,790 a month to a Continuum of Care tenant. I collected 2 months’ rent, which is $5,580, as a security deposit, along with a $1,000 thank you for working with us bonus. Not only that, but I also negotiated that they paid me the next month's rent of $2,790 in advance. They were happy to accommodate my request. So yes, I received almost half of what I had invested into the renovation the day I rented the place.

You can see some before and after photos and the contract as proof. Again, it all comes down to knowing what to do and what Section 8 program would be the right fit for the property and finding the tenant that would be aligned with your overall strategy. And feel free to do the math on the return on investment if you choose.

What I am about to share with you will radically change your thinking about how you invest in buy-and-hold properties. I want to introduce you to a much more sophisticated way of creating income security for yourself in a noisy marketplace of unproven, hyped, or fly-by-night ideas.

I have also authored multiple books on real estate investing. Some of them are used as reference material and found at the libraries of some of the world's most renowned universities. But what's more important for you to know is that everything you are about to learn here comes from my actual experience, not academic theory.

HOW I MADE THE DISCOVERY

Back in 2008, during the market crash, I found myself in the California Bay Area with 56 seemingly "reliable," "well-screened," "high income," and "credit-worthy" tenants who stopped paying rent one after the other.

It was a soul-crushing experience to witness my once-reliable source of income dwindling away.

The mess those tenants created took years to clean up, and I learned the hard way that traits like "reliable" and "credit-worthy" were historical indicators. It told me nothing about how an individual would behave during a crisis.

I began to believe that buy-and-hold as a tactic was not for me and was meant for those who had a ton of cash reserves to ride out inevitable storms. I was convinced that I would have to continue to work for money, exchanging hours for dollars, and the idea of predictable, stable cash flow from rental real estate was unrealistic. My passive income dream was dead.

In the following years, I primarily focused on renovating properties to resell. Pre-foreclosures and short sales were everywhere, and I really sharpened my renovating and assignment skills at that time.

Deep down, however, I really wished for some stability in my income. Something I could rely on month after month. Something that would add certainty to my very uncertain career choice as a real estate entrepreneur. A choice where every day was like waking up to slay a dragon, with no days off. Sometimes, I would win, and the successes would be incredibly rewarding. But the times when the dragon would win, the pain would be unbearable. It was always either feast or famine.

While the positive impact of revitalizing homes and neighborhoods was very fulfilling, with no income security, I had no peace of mind.

A turning point came when I was approached by a fellow investor who had found himself in a financial bind. He needed to offload his entire portfolio quickly. He was willing to offer a substantial discount for a fast closing, which meant we would have almost no time for due diligence.

The portfolio he presented was a mixed bag of single-family and multifamily homes, each with its own set of challenges. Some properties needed significant repairs, others were vacant, and some were rented, producing income. To further complicate everything, the properties were spread out over different states! I didn’t have a problem with the properties needing repairs or the vacant ones. It was the rental properties that I thought were a huge risk.

With my strong real estate appraisal and valuation background, I was able to do some quick analysis, and I figured I would be able to make it work one way or another. I crossed my fingers but didn't hesitate. This wasn’t the time to be timid.

Post-acquisition, I was analyzing the portfolio in depth to figure out the overall strategy and tactics I would use in the process. As I sifted through the deals, I made a discovery that piqued my interest. A handful of the properties in this portfolio were occupied by Section 8 tenants.

As I dug deeper, I found out that the Section 8 tenants didn't require any reminders for payments. The housing authorities automatically made direct deposits on the same day every month.

The payments were consistently received on time, and the rental records were meticulous and well-organized.

The stark contrast between these Section 8 rentals and the other properties in the portfolio was undeniable. The rent collection was a constant struggle with the other properties. It became clear that the properties with Section 8 tenants offered reliability and consistency that was unmatched by the other properties in the portfolio.

As I renovated the properties across the different states, I began working closely with the local housing authorities to enroll additional properties into the program. After months and months of dealing with housing inspectors, and wasting a lot of money, I finally learned what it took to meet the HUD requirements with minimal capital investment instead of over-improving the properties. The inspection requirements were very different from what I was used to when dealing with city inspectors when I renovated homes to sell to retail buyers.

Over time, I also discovered that there were many other little-known programs under the Section 8 umbrella. Combined, these programs provided an endless source of tenants with different rental timelines and objectives. While the mainstream voucher program delivered one type of tenant, participating in the other programs allowed me to diversify my tenant base. But they all had one thing in common: they all were backed by government funding.

Eventually, the portfolio transformed from a chaotic mix of distressed properties into an outperforming asset that I could sell for a substantial premium because of the predictable, reliable cash flow.

I have continued to invest in Section 8 rentals. My investment thesis was put to the test and proven right even recently. During the COVID-19 pandemic, while others struggled with rent collection, my current portfolio of Section 8 rentals continued delivering income with the same predictability.

I will tell you more about my approach to Section 8 investing in a bit. But right now, here’s what we are going to cover next. We’ll be covering 3 secret frameworks.

SECRETS YOU WILL LEARN TODAY

Secret 1 - Section 8 Income Transformer: How to quickly replace your current sources of income with government-sponsored Section 8 rentals.

Secret 2 - Section 8 Rapid Tenant Locator: How to immediately find tenants that are looking to move in and move out based on your timeline for the property.

Secret 3 - Section 8 Rent Maximizer: How to determine the maximum rent the Housing Authority will pay for your unit so you don’t undercharge your tenants.

Here is:

SECRET FRAMEWORK # 1 - SECTION 8 INCOME TRANSFORMER

Remember earlier when I told you about the framework I developed that helps me and my clients acquire Section 8 rentals? Get ready because I’m going to walk you through this framework. I call It the Section 8 Income Transformer. It shows you how to quickly replace your current sources of income with government-sponsored Section 8 rentals.

Like many of you, I read the Rich Dad Poor Dad book by Robert Kiyosaki. I played the Cashflow board game he has created many, many times. In the game, and as per Kiyosaki, when your monthly passive income exceeds your monthly expenses, you are out of the rat race.

Well, that was my objective when I started buying real estate: buying and holding enough real estate with passive cash flow to cover my monthly expenses.

As you have already heard, I purchased rental properties but found regular, reliable tenants who turned out to be not so reliable during a crisis. I ended up losing most of them during the 2008 crash.

A few years later, while I was only focused on rehabbing to resell property, I ended up with a portfolio of assets, many of which were Section 8 rentals. I discovered that the rents were predictable, reliable, and guaranteed by the government, and it helped me achieve my goal of replacing my active income and gaining financial security. Here are the steps for the Section 8 Income Transformer:

Step 1: Determine your active income needs

The first step is to figure out where you are, what your monthly income is, the sources of that income, your monthly expenses, and how those expenses are covered. If you already own rental real estate, some of your income may already be covering some of your monthly expenses. If you are in a negative cash flow position, like many investors, that is a problem property, and you need to address that situation quickly before it becomes a major issue.

Step 2: Source residential deals that get you to that number quickly

Once you have determined how much active income you need to replace, you can reverse-engineer everything. For this to work and work well, you need to source 1 to 4-unit properties and no more than 4 units. These properties could be in your city, in another city, in your county or another county, in-state or out-of-state, depending on your level of experience and comfort with investing. It doesn’t matter.

Step 3: Prescreen the deals for desirability and rental demand

Make sure the neighborhood you pick is desirable to tenants and that there is sufficient rental demand. Some areas are more in demand than others, so it’s best that you check before jumping in.

Step 4: Acquire the deal using conventional or non-traditional financing

You can buy the deal all cash, with conventional financing, government financing, hard money loans, private money loans, subject to the existing financing, or with seller financing. Depending on your experience and your ability to prescreen, you have to make sure that the deal cashflows and moves you towards replacing your active income.

What may motivate you is to address a specific expense line item on your financial review. Say, for instance, your monthly grocery bill is $1,000. You want to find a deal that will generate enough cash flow to cover that monthly payment. Or, say you have a car payment that's $500. You would want to find a deal that would cover that amount.

Step 5: Sustainably Rehab the deal to meet Housing Quality Standards

There are 13 sections that fall under the Housing Quality Standards performance requirements. That’s what they want you to renovate for. Nothing else, so you need to plan for that. This way, you minimize your cash outlay and do only what's needed to pass inspection. You need to make sure that the property is habitable and meets health and safety requirements, which does not mean it needs to look like a palace on the inside.

Step 6: Stabilize the asset with a tenant that meets your hold timeline

You need to know what your hold time is for the property and find tenants accordingly. There are tenants who are happy to live in your unit for decades, and some tenants are ready to move on within a year. Aligning yourself with a program that provides you with tenants that meet your hold timeline is very important, especially if you are planning on selling the unit vacant to an owner-occupant.

So, here’s a quick recap of Secret Framework # 1: The Section 8 Income Transformer

Step 1: Determine your active income needs.

Step 2: Source residential deals that get you to that number quickly.

Step 3: Prescreen the deals for desirability and rental demand.

Step 4: Acquire the deal using conventional or non-traditional financing.

Step 5: Sustainably Rehab the deal to meet Housing Quality Standards.

Step 6: Stabilize the asset with a tenant that meets your hold timeline.

As you have already seen earlier, I still do this successfully for myself and my clients, who own assets in different parts of the country.

Let’s go on to:

SECRET FRAMEWORK 2 – SECTION 8 RAPID TENANT LOCATOR

When I was in the process of stabilizing the real estate portfolio I had mentioned earlier, there was a non-Section 8 tenant couple that unexpectedly moved out in the middle of the night from one of the properties. Their relationship had taken a turn for the worse, leading them to part ways abruptly.

To make matters worse, they left right on the 3rd of the month, and they left without paying their rent. What's more, there was no deposit on file to cover the unpaid rent. Remember, I bought the portfolio as is, where is.

The property was not in the best part of town, and empty homes were frequently vandalized. I knew I had to act quickly to fill the vacancy. I was familiar with the Section 8 program by now, and they were not known for speed. The permanent voucher program could take anywhere from 30 to 45 days to process.

I had a conversation with one of my existing Section 8 tenants, who mentioned that she had a friend actively searching for a place to live. Her friend held a different type of Section 8 voucher – a temporary one. I decided to meet with the friend to learn more about their situation and the temporary voucher program. During my conversation with the friend, it became clear that this voucher type offered a much faster process for both tenants and landlords. According to the tenant’s case worker, if the property passed inspection, the turnaround time for approval and move-in could be approved in a few days, if not the same day.

I later found out that some of the temporary voucher programs even offer you 2 months' worth of rent as a security deposit, which was a lot more than any of my reliable tenants ever paid me. This was incredibly different than the permanent voucher program in both speed and flexibility.

Here's the framework for the Section 8 Rapid Tenant Locator

Step 1: Determine your hold timeline for the property.

Many investors get into a deal and never think about this. What is the property going to achieve for you? Do you want it to replace your active income? Do you want it to help you pay for a new car? Pay for your yearly vacations? What's the reason you are looking to bring this deal into your life, and for how long? Are you looking to stabilize the asset, enjoy the cash flow for a few years, and resell? This will be a crucial factor in tenant selection.

Step 2: Identify your exit strategy.

Would you be okay building a portfolio to sell to another investor who is looking for cash flow so you can make a huge multiple for the stability of the cash flow? Would you consider selling the property to the current tenant? They are already backed by the government, so that may be a viable option. Are you looking to sell in a year? Are you looking to hold on to it for the long term? Long term being 10 or 15 years? Are you looking to create an opportunity for both capital gains and cash flow? Those are the things you should ask yourself.

Step 3: Connect with the different housing agencies.

Once you have clarity on your hold timeline and exit strategy, you can start thinking about what type of tenants you want. There are many organizations in Section 8, and you need to familiarize yourself with them. Some work with temporary vouchers, and some with permanent vouchers. Some have the funding for the tenants to eventually buy the property, and some don't. Some have tenants that will move within 30 days, some have tenants who can move in right away. Connect with them so they can send you the tenants that will work with your objectives.

Step 4: Prescreen your tenants.

The last thing you want is a tenant who is looking for a temporary situation and offer them a permanent housing solution or vice versa. When a housing agency sends you a tenant, you want to make sure they are aligned with you from the beginning while staying flexible and reasonable so there are no misunderstandings. You will also need a bulletproof lease agreement that helps you enforce this as well. Include specific lease terms in the rental agreement regarding the duration of the lease, any renewal options, and how the Section 8 voucher will be handled if the tenant's circumstances change.

Here’s a quick recap of Secret Framework # 2: Section 8 Rapid Tenant Locator

Step 1: Determine your hold timeline for the property.

Step 2: Identify your exit strategy.

Step 3: Connect with the different housing agencies.

Step 4: Prescreen your tenants.

Let’s go on to:

SECRET FRAMEWORK 3 - SECTION 8 RENT MAXIMIZER

While I really appreciated the consistent rental payments from the Section 8 properties, there were a few things that really bothered me about the existing arrangement.

The investor who sold me the portfolio had owned the properties for a while, and over the years, he never bothered to increase the rent. Even worse, he had included all the utilities in the rent payment, so he would be responsible for paying for it from his cash flow! I figured he thought this good deed would grant him a special place in heaven.

The soaring water bills on some of the multifamily properties, combined with the low rents, were pushing me into a negative cash flow territory. Additionally, a lot of the appliances in the properties were old, so there were constant repair and maintenance issues that I had to deal with.

I went on a mission to become water-efficient and replace all the toilets and faucets with water-conserving fixtures so I could save some money on a monthly basis. The capital expense was a tough pill to swallow, but I figured it would be worth it. While the appliances needed repairs and were a maintenance headache, they didn’t warrant replacement. Mostly because there was no money left for it! The water bills, however, were a consistent monthly headache, and something had to be done.

A few months later, after installing water-conserving fixtures, I reviewed the bills again and was shocked to see that the water bill was only slightly lower, if not the same. After investigating further and doing some detective work, I found out that some of the tenants had turned their driveways into community car washes, and some basements had been turned into laundromats for friends, families, and even neighbors! While I couldn’t do anything right away since I had to honor the existing lease, I figured I would renegotiate this at the time of renewal.

At the time of renewal, I found out that who pays for utilities was negotiable, which meant that I didn’t have to be responsible for the water or electric bills if there were separate meters! Utility companies actually had programs to subsidize the utility bills for these tenants to almost nothing, so there was no reason for me not to make this change. So now, if a tenant wanted to run a car wash from the property or do the neighbor’s laundry, I wouldn’t be stuck with the bill.

In situations where the meters were not separate, as they are in multifamily, I was able to ask for a higher rent from Section 8. Not only that, but I also found out that I didn’t even have to provide the appliances. Yes, not even the fridge or the stove! It was not required, and if I did decide to provide them, I could charge a higher rent.

I also learned about the Payment Standards and Fair Market Rents and how they affect how much rent you can charge. Some Housing Authorities were flexible and reasonable when it came to bringing up the rents to match the current market, and others weren’t.

After a few iterations and a lot of mistakes, I finally came up with a framework that I could use to maximize my cash flow. As the leases came up for renewal, the changes were implemented. The results were astounding. My monthly cash flow received a much-needed boost, and I was no longer in the red.

Here are the steps for the Section 8 Rent Maximizer

Step 1: Confirm that the unit size matches your bedroom count

The unit size is stated on the voucher the Housing Authority provides to the tenant, and it is determined by the tenant's family size. It dictates the maximum allowable rent that the Section 8 program will cover. So, if your tenant has a 2-bedroom unit size stated on their voucher and you have a 3-bedroom unit, you will not be able to get Section 8 to offer you rent for a 3-bedroom unit. They will only cover the tenant up to a 2-bedroom unit. Then, it's up to the tenant to pay you the difference, if they can, based on their current income. Otherwise, the Housing Authority will not approve the rental. If you go this route, you will likely be leaving money on the table.

Step 2: Determine the Payment Standards for your unit

Once you know the unit size, determine the payment standard for your unit that has been set by the Housing Authority. The amount may vary by zip code or be the same for the entire area.

Step 3: Determine the Utility and Appliance Allowance for your unit

Based on your unit size, you should figure out what the utility and appliance allowances are for your unit. This will give you additional insights into whether you want to provide certain appliances or what you can expect to be paid to you if you include all the utilities.

Step 4: Confirm the tenant’s income

The tenant’s income makes a difference in the total rent that you can collect. The Housing Authority has controls in place to make sure the tenant’s rent burden is within reason, and they don’t break their promises. So even though you may want to charge more, a Housing Authority will not approve the tenancy if the rent is over certain thresholds.

Here’s a quick summary of Secret Framework # 3: Section 8 Rent Maximizer

Step 1: Confirm that the unit size matches your bedroom count.

Step 2: Determine the Payment Standards for your unit.

Step 3: Determine the Utility and Appliance Allowance for your unit.

Step 4: Confirm the tenant’s income.

So let me ask you a question.

If you followed what I showed you in Secret # 1 and identified a property that would make a great candidate to quickly replace your current sources of income with Section 8 income.

Then, you did what I showed you in Secret # 2 and rapidly located tenants who are looking to move in and move out based on your timeline for the property.

And then, you used Secret #3 to rent your properties out to Section 8 tenants and charge the maximum rents allowable by the Housing Authorities so you don't leave any money on the table, do you think you could be successful?

Are you feeling excited about what we just went over? Are you feeling a little overwhelmed because we've covered so much? Well, that was a lot of information!

If you are ready to move forward and want to implement this new opportunity, I have some information for you.

By the way, if none of this felt relatable or doable to you or you don't want to learn more, that's totally okay. But if you are interested in learning more, I am going to share a very special offer I created to help you Invest in Section 8 Rentals. A system that will help you rapidly replace the income from your job and the stock market during these turbulent times. It’s called:

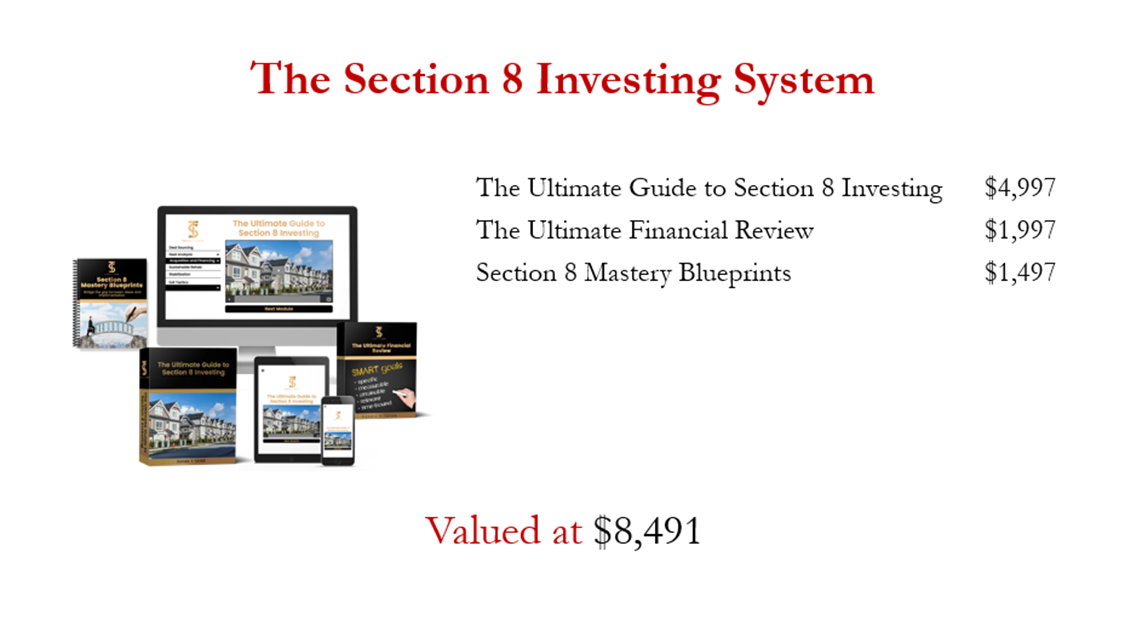

THE SECTION 8 INVESTING SYSTEM

Here’s the first part of the offer:

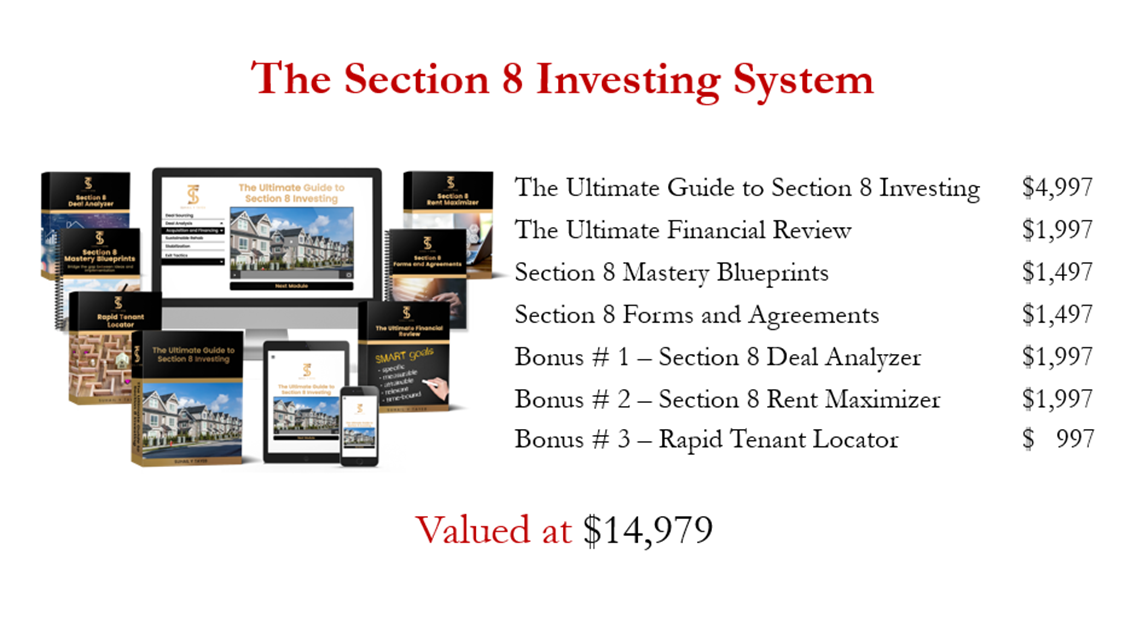

The Ultimate Guide to Section 8 Investing Training

This comprehensive 6-module training walks you through the entire lifecycle of a Section 8 rental. You train with me through a combination of live and recorded sessions. You get to watch the training videos, and then we regroup for a live session and discuss what you learned and how you are going to implement what you learned and get it to work for you.

What I have done with this training is share everything I would do if I were starting from scratch. I discuss what I would pay attention to and what I would avoid based on my experience with the Housing Authorities, the different types of tenants, and the different types of buyers of such properties. I would begin with the end in mind.

I had to go back years and review all the mistakes I had made, all the oversights, everything that went right, and everything that went wrong and distill it down for you so you can become successful quickly instead of wasting time. Here’s what the training covers:

In Session 1, we discuss Deal Sourcing: How to find properties that are best suited for Section 8 rentals and find deals that would work best for your situation.

In Session 2, we go over Deal Analysis: How to analyze the deal so you have multiple exit opportunities. We cover prescreening, entry and exit valuation, and what makes a good investment.

By Session 3, you are ready to talk about Acquisition and Financing. We discuss the different ways to structure the terms of acquisition and where to find the money to do the deal in case you want to raise private money.

In Session 4, we cover the Sustainable Rehab. This is how to renovate the property and avoid the over-improvement trap. I’ll tell you what you need to fix and what you don’t need in a home so you can avoid and minimize maintenance headaches. I’ll show you how to meet Housing Quality Standards requirements without breaking the bank.

Session 5 is about how to stabilize the property with the right tenants. We go over how to find the right program for your property and your timeline, lease agreements, Housing Authority applications, and dealing with property management issues. We discuss how to market the property for tenants and how to determine the maximum rents you can charge to optimize your cash flow.

In Session 6, we will discuss the Exit and talk about the different ways you can exit a deal and how to get ready to sell.

So that’s the first item in the System and it’s valued at $4,997.

When you enroll in the training, not only will you save the money that I spent to learn all this, but you will also save what could be months or years because you'll be doing it right the first time. There is no trial-and-error period.

So, I want to go back and make sure you realize who this is for.

It's for people who currently own or manage real estate or are in the market to acquire real estate. It could be your first property, but you must have the ability to either raise capital or already have the capital to do the deals. It is not for someone who is really starting out with no cash, no credit, and, more importantly, no training.

But wait a minute Suhail, you just showed us a deal where you got 100% seller financing. Why do I need to have money to do deals? Well, good observation, that is correct. But guess who paid the closing costs? I did. Who paid for the renovation? The private lender did. So, you need to have some cash to be able to do these deals or have access to some capital. If you don't right now, don't get disheartened, there are plenty of other tactics you can use to make some cash. This isn’t the right tactic for you just yet.

Let’s cover the next item you get in the offer:

The Ultimate Financial Review

Regardless of how seasoned or new you are to real estate, this is where you should start. With the Ultimate Financial Review Software Tool, you will go through a simple process, after which you gain incredible visibility into where you are today and what your next steps should be to get to the next level with your investing.

If there were one thing I wish I had when I first started out as an investor, it would be this training. When my private coaching clients sign up to study with me, regardless of their experience level, they all have to go through this process. No exceptions. Even as a seasoned investor myself, I constantly go back to this tool to gain insights and how an investment decision will affect my overall strategy.

You’ll experience a marked improvement in your decision-making skills, and you will learn to focus on the opportunities that are right for you and not on those that take you away from your goals. As Steve Jobs famously said, “People think focus means saying yes to the thing you've got to focus on. But that's not what it means at all. It means saying no to the hundred other good ideas that there are.”

In Session 1, we do an Assets Review, which looks at what assets you own and their current performance.

In Session 2, we do a Liabilities Review. We determine what you owe to whom and when it's due.

In Session 3, we discuss all your monthly Income Sources.

In Session 4, we discuss all your Monthly Expenses, when they are due, and how they are being covered.

By Session 5, you are ready for your Financial Summary. We will analyze your dependence on Active Income and the various ways we can minimize the dependence on it.

Session 6 is all about Setting SMART Financial Goals, which are specific to you, measurable, achievable with the right guidance, relevant to your overall strategy, and time-bound to when you need to achieve the goals, so you have a way to measure progress.

In Session 7, we Strategize to Achieve Those Goals with The Right Tactics that make sense for you.

So that’s the second item in the System, and it’s valued at $1,997. Bringing us to a total of $6,994.

Let’s look at what else is included.

Section 8 Mastery Blueprints

I enjoy case studies, and I learn a lot faster when I have case studies that I can review over and over again.

With the Mastery Blueprints, you get just that. You will bridge the gap between ideas and implementation through various case studies. You get to learn from a combination of those who went before you through actual cases in different parts of the country in high- and low-priced markets.

The case studies may be very similar to your own situation and deals that you are looking at, so you will learn how to execute the deal successfully.

So that’s the third item in the System, and it’s valued at $1,497. Bringing us to a total of $8,491.

Let’s look at what else is included. The next item is:

Section 8 Forms and Agreements

Remember in Secret # 3, I talked about the importance of getting a utility allowance so you can maximize your rent? Well, if you currently have a Section 8 tenant and you are the one currently paying the utilities, there are specific forms that you need to use and provide to the Housing Authority to make that request and get that changed. All of that is included here, along with the process. If you are looking to learn how to sell your property to the Section 8 tenant, that’s in here, too.

There are also other various forms, lease agreements that protect your interest, rent guidelines, utility allowances, notices, inspection checklists, housing standards requirements, and disclosures that are involved in the Section 8 rental process that investors should be familiar with, or they risk getting caught off guard. The Section 8 Forms and Agreements manual has you covered.

So that’s the fourth item in the System, and it’s valued at $1,497. Bringing us to a total of $9,988.

Let’s look at what else is included. The next item is:

Bonus # 1 – Section 8 Deal Analyzer

If you have ever felt stuck making a go- or no-go decision on a deal, the Section 8 Deal Analyzer will fix that for you. I took the entire process that I have been using for years out of my mind and put it on paper. Then I had a developer build it out based on what I would do to make the deal work and all the items I was checking off in my mind and put it in a system to create the Section 8 Deal Analyzer. It makes sure you don’t overlook anything if you need to make a decision quickly. You’ve got to admit computers are way better at following the process than we are. No more wondering if a deal makes sense or not. By using the Section 8 Deal Analyzer, you will be able to quickly determine if a deal is in line with your overall strategy.

The Deal Analyzer starts by analyzing the transaction drivers, including the rents that the local housing authorities will pay for your type of unit, and works backward so you can reverse engineer your acquisition. The tool also reviews the balance sheet for your property and the monthly property income statement to review or project operating expenses so you can track your financial performance.

It also allows you to explore various scenarios, such as selling the property or doing a cash-out refinance after stabilizing the asset. This feature helps you plan and consider different exit strategies. The risk assessment feature of the tool factors in potential risks associated with your Section 8 investment, such as vacancies and maintenance costs. Assessing these risks allows you to make informed decisions and develop mitigation strategies.

So that’s the fifth item in the System, and it’s valued at $1,997. Bringing us to a total of $11,985.

Let’s look at what else is included. The next item is:

Bonus # 2 – Section 8 Rent Maximizer

Remember the framework I shared with you in Secret Framework # 3? Well, I took my entire process and put it into software so you don’t make any mistakes or leave money on the table.

By being informed about what the Housing Authorities would be willing to pay you, you maximize your returns and simplify your decision-making process. By charging Market Rents like other landlords, you may be hurting your cash flow.

The Rent Maximizer uses the information based on the voucher, the tenant’s income, and the local utility and appliance allowances, which allows you to factor these expenses into your rental pricing strategy. The tool features an intuitive and user-friendly interface that makes the process a breeze.

So that’s the sixth item in the System and it’s valued at $1,997. Bringing us to a total of $13,982.

Let’s look at what else is included. The next item is:

Bonus # 3 – Rapid Tenant Locator

Rember Secret # 2, where I talked about finding the right tenant for your property? Well, do you want to find tenants through agencies that are happy to pay you 2 months’ worth of rent as a security deposit? How about the ones that pay you a nice signing bonus? How about ones that even offer to pay you money to do some of your repairs to meet the Housing Quality Standards? Maybe you want to sell your property to your tenant. Do you want to learn how you can do that, and through what programs? The Rapid Tenant Locator can show you how.

A lot of times, even the agents at the Housing Authority don’t know about all the different programs they may have available. You must talk to the right people for that. This program tells you who you need to talk to at the Housing Agency to get heard and expedite your process.

The Rapid Tenant Locator helps you find tenants that match your objective and whose timeline matches your timeline for the property. These tenants will move in when you want them to and move out based on your plan for the property. You will learn about the different government-sponsored tenant programs that you can leverage to expand your tenant pool.

So that’s the seventh item in the System and it’s valued at $997. Bringing us to a total of $14,979

So, let’s go over everything you will get when you enroll in The Section 8 Investing System today:

LET’S RECAP THE OFFER

If all this package did was find you one deal that generates $1,000 a month cash flow till you own it, and replace $1,000 from your active income, would it be worth $14,979?

Now, even though I should, I'm not going to charge you $14,979. But if I DID charge you $14,979, and all it did was help you gain $400 a month more in cash flow by charging the right rent, would it be worth it to you?

If all the package did, was fill your vacancies 30 days faster, saved your home from vandalism, saved you money on rehab costs, and fetch you a premium when you sell for the incredible stability of the cashflow, would it be worth $14,979? You bet it would.

I had two choices with this. I could go as cheap as possible and try to sell as many as possible. But the problem with that is I couldn't really stack the value for you. So, I decided to go with a second option, which obviously requires a slightly higher investment on your side. But in exchange for that, my team and I can dedicate more time, energy, and resources to help guarantee your success.

So, if you were able to replace your active income or supplement your income with a government-backed rental program that was bringing in money consistently every month, and you don’t have to depend on your active income anymore, what would it be worth to you?

How much would you pay to have that one property or that portfolio of properties, all with government-guaranteed rent?

You can probably see why people pay $30,000 to come to work with me in person for a similar result because it’s not a cost. It's an investment.

You've already seen how it's worth $14,979, but I am going to give you a very special offer since you are investing in yourself.

You can get this training today for just $1,497.

I know I could have priced it a lot higher, but I know what people are going through. The income insecurity problem is very real, unfortunately. It is my hope that my program allows you to gain a sense of financial security in these uncertain times.

The way I see it, you’ve got two choices. You can either learn from the school of hard knocks, which is very, very expensive, or you can make an investment in yourself and learn from someone who is willing to share their knowledge and experience.

There is even a remarkably generous DOUBLE GUARANTEE.

UNCONDITIONAL 60-DAY MONEY-BACK GUARANTEE

Your first guarantee: You have TWO full months to examine everything, use what you wish, and if for any reason, or even no reason, you want a full refund, just return everything, and you’ll get your money back immediately. No questions asked.

You do not need a “my dog ate my homework” story. No one will ask you any questions at all. No hassle. No “fine print”. Simple and straightforward. You are thrilled with what you get in my System, or you get a full refund. And, incidentally, I’m devoted to the goal of having only satisfied customers. If you are not going to profit from having my System, I really would prefer to buy it back.

CONDITIONAL 12-MONTH MONEY-BACK GUARANTEE

Your SECOND Guarantee: If you keep the System after the two months, I'll ride along with you for another TEN months, and if, after a full year from your purchase date, you will show me proof that you used at least one tactic or tool from the System, and you will look me in the eye on paper and tell me you did not replace any of your active

income or put at least $10,000 in your bank account that you would not have otherwise, send me a note describing your use and failure with the System, and I will STILL refund every penny you've paid - even after one full year.

I want you to put tens of thousands of dollars of income in your bank account that you know would never have gotten there without my System, or I want to buy it back.

FAST ACTION BONUS

An Incredibly Valuable Fast Action BONUS Offer:

I've also reserved a copy of my Special Report, "The 3 Most Common Mistakes Investors Make When Renting to a Section 8 Tenant," that you get as part of the program. You keep that Report even if you choose to return everything else for a refund.

So, TWO FULL MONTHS, unconditional satisfaction guarantee. PLUS, an additional TEN MONTHS conditional guarantee PLUS the Bonus Report, yours to keep regardless of your decision about everything else.

Click the link below to get your Section 8 Investing System at a very special discounted price.

THE SECTION 8 INVESTING SYSTEM